As we write this newsletter, there is definitely no shortage of topics to write about, but it is much more difficult to formulate conclusions to what we have seen recently. Time and hindsight give us perspective that sometimes is lacking in the heat of the moment.

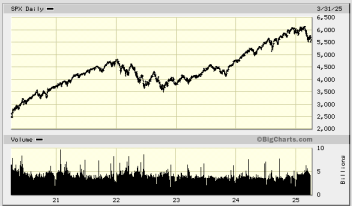

Some newsletters are easy to write and almost write themselves. Take our January newsletter, we had just completed back-to-back 20%+returns years in the stock market and had an election. We had no shortage of topics to write about. As we write this newsletter, there is definitely no shortage of topics to write about, but it is much more difficult to formulate conclusions to what we have seen recently. Time and hindsight give us perspective that sometimes is lacking in the heat of the moment. Before we jump into details, I think it is extremely important to put things in perspective. Below is a chart of the S&P 500 from March 31, 2020 (COVID) to March 31, 2025 (Tariffs).

The S&P 500 wrapped up the first quarter of 2025, down 4.6% and breaking a 5-quarter win streak. The Nasdaq did even worse, with a 10.4% pullback this quarter, its worst 3- month performance since 2022. When we look at the first quarter only, investors started to panic at the sell-off. Increase the time period as I did above, and we are not even back to January 2024, and we are still double where we were just 5 years ago.

After a small increase in the S&P 500 to start the year, the market dropped as we approached the inauguration. President-elect Trump had indicated he would implement tariffs on his first day in office. When he did not, the market rallied over 5% and traded in a range around that level as tariffs were announced against Canada and Mexico.

While the stock market was volatile in the first quarter, gold broke through to another all time high, oil rose back above $70 per barrel and the Bloomberg U.S. Aggregate Bond index gained 2.8%. The 10-year Treasury yield ended the quarter at 4.2% after reaching 4.8% in January. European and other developed markets represented by the MSCI EAFE gained 6.1%, and emerging markets represented by the MSCI EM gained 2.4%.

Looking at the U.S. economy, inflation, as measured by the Consumer Price Index, increased slightly to 2.8% in March. The unemployment rate remained low at 4.2%, and measures of Consumer Sentiment fell to its lowest level since 2022. The Federal Reserve met and kept interest rates the same and warned of increased inflation later in the year.

The first quarter of the year can be summed up and will be remembered by one word, tariffs. To avoid a political debate, we will go with the definition in the dictionary:

tar·iff

noun: tariff; plural noun: tariffs

a tax or duty to be paid on a particular class of imports or exports.

Tariffs have been around throughout history and date back in the United States to The Tariff Act of 1789. The most well-known tariff act is the Smoot-Hawley Tariff Act of 1930. Tariffs are usually assessed on individual products entering the United States, the company importing the item pays the tariff and typically increases the price of the item sold to offset the tariff that was paid.

We are going to avoid speculating on what the effect of the tariffs will be on the United States economy, as it is to early to know. Both political parties are predicting very different outcomes, and we anticipate that we will address those outcomes in future newsletters as it pertains to investments.

Paragon is focused on the differing impacts of tariffs on the earning and future prospects of the companies we follow and the overall markets. We will also be closely following volatility as measured by the VIX index, the VIX is one key component of pricing Structured Products. The more volatility and higher the VIX, the better the terms on the notes we create for our clients.

Stagflation

Beginning in February, some economists were predicting the potential for stagflation, so what is it? In simple terms it is an economic condition characterized by simultaneously high inflation, slow economic growth, and high unemployment. In March we saw inflation rise more than expected and consumers spent less than expected. The anticipation is that unemployment will rise with government layoffs and corporate layoffs due to tariffs. We haven’t seen that number move enough yet to get to stagflation, but the markets move in anticipation of events happening. For now, we will keep an eye on inflation and consumer spending. The Federal Reserve still anticipates two rate cuts this year, which would be problematic for inflation but would help with consumer spending.

Liberation Day and the Impact on the 2025 Outlook

Two days into the second quarter, the current administration announced a new tariff regime on what they have termed “Liberation Day.” While the market had priced in what was expected to be an across-the-board 10% tariff, the administration took an alternate approach and announced varying tariff levels based on the current trade deficit with the given country. In short, the administration laid out a new global tariff regime that was harsher than the market had expected, and the markets reacted poorly. The VIX has doubled, long-term interest rates are down, and equity markets have pulled back roughly 10% in the aftermath of the announcement.

Our clients, business leaders, and others reading this newsletter are concerned about the headlines and the impact these announced changes will have on their businesses and their portfolios. We would love to say that we have the “magic answer” to calm investor nerves, but there are still many questions that need to be answered. At this time, global leaders and the current administration are considering their next moves and ultimately nobody knows if this marks the peak in tariff pressure or if things will get better or worse from here. Uncertainty will most likely remain high in the coming weeks and months, leading to sustained levels of high volatility as measured by the VIX as the markets react to every twist in the wind.

We are NOT recommending that our clients panic at this time and make broad changes to their asset allocations. We are taking advantage of the higher levels of volatility in the market and creating structured notes with attractive terms for the benefit of our clients. In the equity markets we are taking advantage of the more attractive valuations and buying equities for our clients where it makes sense. We will continue to monitor the impact of the announcements on markets and make adjustments as necessary. For those reading this that are not clients, I would recommend talking to an investment advisor and if you don’t have one, we would be happy to speak to you about your portfolio or give you a second opinion.

Recap

Howard has been advising clients since the 1960’s, Craig since the mid 1990’s, while the rest of our team has over 20 years of experience in the markets as well. Howard guided clients through Black Monday (1987), while Howard and I, and the rest of the team have guided clients through the Technology Bubble (2000), the Global Financial Crisis (2008), and Coronavirus (2020) and all the ups and downs along the way. During each of these time periods, there has been a sense by investors that things could only get worse and markets would never recover. We cannot tell you how long this will last or how deep any correction may become, but we believe staying the course, making tactical adjustments as they present themselves, and in time markets will recover and move to new highs. We are here to advise, counsel, or just listen! Please reach out with any concerns or questions, we are always happy to talk to you.

How to stay informed

Our website and YouTube channel offer a wealth of information. You can find our videos through our website at: https://www.paragoncap.com/quarterly-market-insights

or on our YouTube channel at https://youtube.com/@paragoncap. If you subscribe to our YouTube channel by hitting the “subscribe” button, you will be notified when new videos are posted.

In addition, for up-to-date news and thoughts from Paragon, plus interesting articles on current topics, we encourage you to follow us on LinkedIn and/or Facebook (links below). We have company pages for both and appreciate your liking and/or following us.

• Paragon LinkedIn: https://www.linkedin.com/company/paragoncapitalmanagement llc/?viewAsMember=true

• Paragon Facebook: https://www.facebook.com/Paragon-CapitalManagement llc352968418169300

• Paragon YouTube Channel: https://www.youtube.com/@paragoncap • Craig Novorr LinkedIn: https://www.linkedin.com/in/craig-novorr1a8a822/www.paragoncap.com

Also, please share your experiences with friends and family; we love the opportunity to help those you know with their financial success.

Whether you feel as if you’ve outgrown your advisor or you just want a fresh perspective on portfolio strategies in our current market, our team of experts is here for you.